Buying a home is one of the most significant financial decisions you will make. In a market where closing costs and down payments drain liquidity, a cash back rebate offers a critical financial buffer. According to recent industry analyses, buyer rebates can return up to 1.5% of the purchase price directly to the buyer at closing. This guide explains the mechanics of these rebates, the regulatory framework in Ontario, and how to secure this benefit with an experienced professional.

What Is a Cash Back Rebate?

A cash back rebate in real estate is a portion of the real estate commission that the buyer's agent agrees to return to the buyer after the transaction closes. This is not a discount on the home price. It is a financial incentive provided by the brokerage to attract clients. Cash back rebate is a financial incentive provided by the brokerage to attract clients.

These rebates are typically calculated as a percentage of the purchase price. For example, a common structure involves returning a specific amount for every million dollars spent. This mechanism allows buyers to offset closing costs, such as land transfer taxes, legal fees, or home inspections. It effectively reduces the net cost of acquiring the property. (Cash Back Realtor Dan)

Understanding this concept is vital for first-time buyers who may struggle with upfront capital. By leveraging a rebate, you keep more money in your pocket. This strategy is particularly effective in competitive markets like Mississauga and Oakville, where every dollar counts. (Cash Back Realtor Dan)

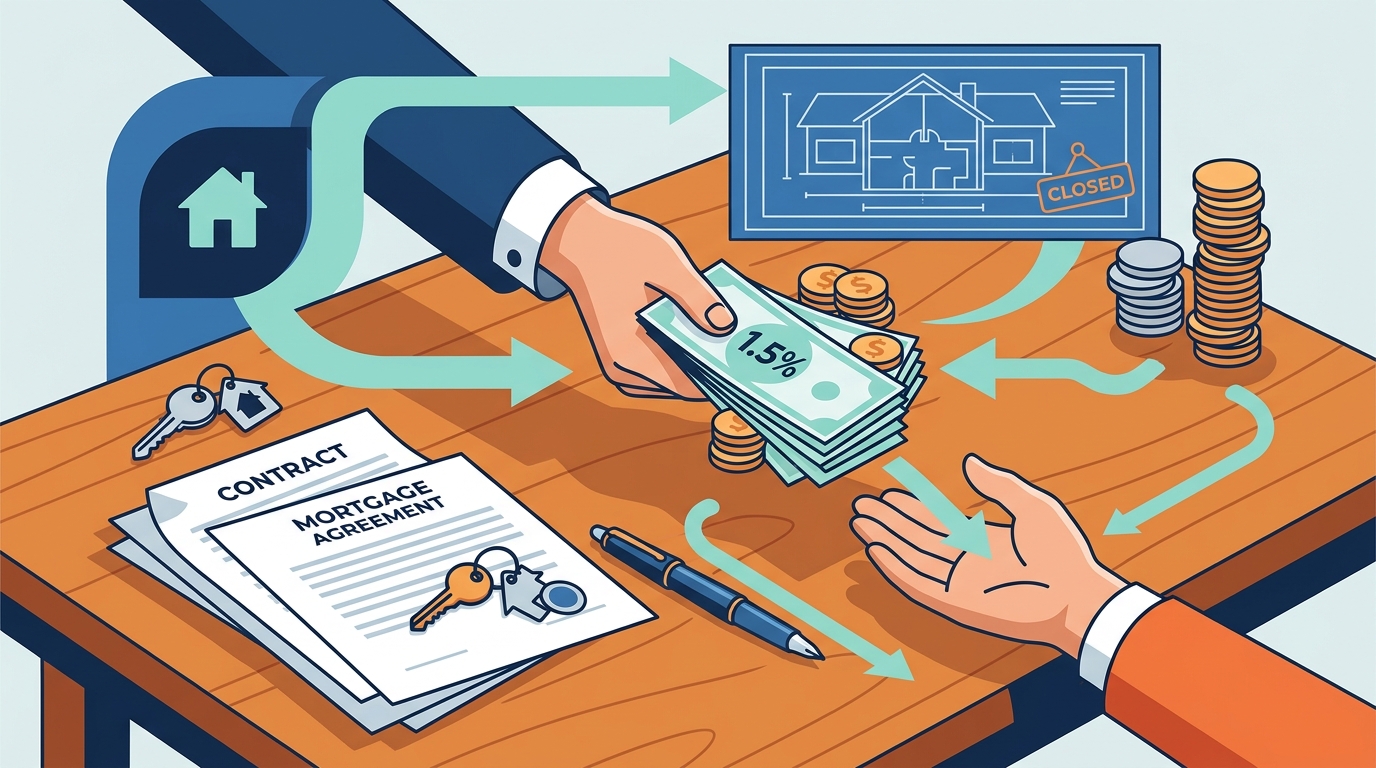

How the Mechanism Works

The process begins with the listing agreement between the seller and the listing brokerage. The seller agrees to pay a total commission, often split between the listing agent and the buyer's agent. In many standard transactions, the co-operating commission offered to the buyer's side is around 2.5%. The co-operating commission is the portion of the seller's fee paid to the buyer's agent.

Here is the step-by-step breakdown of how you receive the money:

- Agreement: You retain a buyer's agent who offers a rebate clause in the representation agreement.

- Offer: Your agent submits an offer on a home that has a sufficient co-operating commission.

- Acceptance: The seller accepts the offer, triggering the commission structure.

- Closing: At the closing table, the listing brokerage pays the total commission to the buyer's brokerage.

- Disbursement: The buyer's brokerage retains a portion to cover operational costs and pays the remainder to you as a cash back rebate.

This process is seamless for the buyer. You do not need to pay the rebate upfront. The funds are disbursed at the time of closing, directly reducing your out-of-pocket expenses. For a home purchased at $1,000,000, a 1.5% rebate results in $15,000 returned to you. This is a substantial sum that can cover legal fees, moving costs, or even home renovations.

Ontario Regulatory Framework

In Ontario, the legality of cash back rebates is governed by strict regulations. The Real Estate Council of Ontario (RECO) oversees all real estate professionals in the province. RECO is the regulatory body that oversees all real estate professionals in Ontario.

Under the Trust in Real Estate Services Act (TRESA), rebates are permitted but must be handled with transparency. The rebate must be disclosed in the representation agreement between you and your agent. It cannot be contingent on you using specific third-party services, such as mortgage brokers or home inspectors. This ensures that your choice of service providers remains independent and unbiased.

Both the brokerage and the agent must be licensed and insured. Green Hedge Realty Inc., Brokerage, and agents like Dan Darragh operate under these strict guidelines. This regulatory oversight protects consumers from predatory practices. It ensures that the rebate is a genuine financial benefit and not a trap for additional fees.

Furthermore, the rebate is considered taxable income in some contexts, though it often offsets the cost of the home purchase. It is advisable to consult with your accountant regarding the tax implications. However, for most buyers, the immediate cash flow benefit outweighs any minor administrative complexities.

Eligibility and Requirements

Not every home purchase qualifies for a cash back rebate. The primary requirement is the co-operating commission offered by the seller. If the listing brokerage offers a low commission, there may be insufficient funds to provide a rebate. The co-operating commission offered by the seller is the primary requirement for a rebate.

Typically, a co-operating commission of 2.5% or higher is necessary to support a 1.5% rebate to the buyer. This leaves a small margin for the buyer's brokerage to cover administrative costs. In markets where commissions are compressed, finding a rebate-friendly agent becomes more challenging.

Additionally, the rebate is usually available for residential properties. This includes detached homes, semi-detached houses, townhouses, and condominiums. New construction properties may have different commission structures, so it is essential to verify eligibility early in the process.

There are no hidden fees or ongoing obligations associated with these rebates. You receive the full benefit without restrictions. The key is to work with an agent who is transparent about their rebate policy from the start. Dan Darragh provides clear, upfront calculations to help you understand exactly what you will receive.

Comparing Rebate Options

When selecting a real estate agent, it is important to compare the value proposition. Some agents offer lower commissions but provide less service. Others offer full service with a rebate. The following table outlines the typical differences.

| Feature | Standard Agent | Rebate-Focused Agent |

|---|---|---|

| Commission Structure | Standard full commission | Reduced commission with rebate |

| Buyer Benefit | None | Cash back at closing |

| Service Level | Full service | Full service |

| Transparency | Variable | High |

Choosing a rebate-focused agent does not mean you receive less service. In fact, many agents offering rebates provide the same comprehensive support. They simply pass on the savings to you. This model aligns the agent's success with your financial benefit.

It is also important to look at the agent's experience and local knowledge. Dan Darragh has over 37 years of experience in the Mississauga and Oakville markets. This deep expertise ensures that you get the best price for your home, which often outweighs the value of a small commission difference.

Key Takeaways

- Financial Impact: A 1.5% rebate on a $1,000,000 home equals $15,000 in cash back.

- Regulatory Compliance: Rebates are legal in Ontario under TRESA and RECO guidelines.

- No Hidden Fees: There are no ongoing obligations or hidden costs associated with the rebate.

- Experience Matters: Dan Darragh has been licensed since 1987, providing decades of market insight.

- Service Quality: Full-service representation is provided without compromising on support.

- Local Expertise: Specialized knowledge in Mississauga and Oakville neighborhoods ensures better outcomes.

- Transparency: Clear communication about rebate amounts and conditions is standard practice.

Frequently Asked Questions

Is a cash back rebate legal in Ontario?

Yes, cash back rebates are legal in Ontario. They are regulated by the Real Estate Council of Ontario (RECO) under the Trust in Real Estate Services Act (TRESA). The rebate must be disclosed in the representation agreement.

How much cash back can I receive?

The amount depends on the purchase price and the co-operating commission offered by the seller. Dan Darragh offers a 1.5% cash back rebate for every $1,000,000 of the purchase price, provided the listing brokerage pays a 2.5% co-operating commission.

Do I have to use specific service providers to get the rebate?

No. You are free to choose your own mortgage broker, home inspector, and lawyer. The rebate is not contingent on using any specific third-party services.

When do I receive the cash back?

The cash back is received at closing. The funds are disbursed by the brokerage directly to you on the day you purchase the home.

Are there any caps on the rebate amount?

There is no cap on the rebate amount. The rebate scales with the purchase price. The more you spend, the more you receive, with no upper limit.

Does this apply to new construction homes?

Eligibility for new construction homes depends on the builder's commission structure. It is best to consult with your agent to determine if a rebate is applicable for a specific new build.

How is the rebate calculated?

The rebate is calculated as a percentage of the final purchase price. For example, a 1.5% rebate on a $1,000,000 home results in $15,000. The exact amount is detailed in your representation agreement.

Contact Dan Darragh

Ready to buy your next home and keep more money in your pocket? Dan Darragh offers expert guidance and a transparent cash back rebate program. With decades of experience in Mississauga and Oakville, he ensures a smooth and profitable buying experience.

Contact Dan Darragh today to schedule a consultation. Let's discuss your home-buying goals and calculate your potential cash back rebate. Visit the Cash Back Calculator to see exactly how much you can save.